As filed with the Securities and Exchange Commission on June 15, 2021

Registration No. 333-256487

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

to

FORM S-1

REGISTRATION

STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 6770 | ||||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification No.) |

Telephone:

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Julio A. Torres

Chief

Executive Officer

Calle 113 # 7-45 Torre B

Oficina 1012

Bogotá, Colombia

(646) 565-3861

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Douglas S. Ellenoff, Esq. Stuart

Neuhauser Esq. |

Paul

D. Broude, Esq. Foley & Lardner LLP 111 Huntington Avenue Boston, Massachusetts 02199 (617) 342-4000 |

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | ||

| Non-accelerated filer ☒ | Smaller

reporting company |

||

| Emerging

growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

CALCULATION OF REGISTRATION FEE

| Title of Securities to be Registered(1) | Amount

to be Registered(2) | Proposed Maximum Offering Price per Share(3) | Proposed Maximum Aggregate Offering Price | Amount

of Registration Fee(4) | ||||||||||||

| Class A Common Stock, par value $0.0001 per share | 5,609,398 | $ | 10.18 | $ | 57,103,672 | $ | 6,230 | |||||||||

(1) These securities are being registered solely in connection with the resale of common stock by certain selling stockholders (the “PIPE Investors”) that entered into subscription agreements with the registrant, pursuant to which the registrant agreed to issue and sell to the PIPE Investors, in private placements that are expected to close simultaneously with the closing of the registrant’s previously announced initial business combination, an aggregate of up to 5,609,398 shares of its Class A common stock, par value $0.0001 per share (the “Common Stock”).

(2) Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the securities being registered hereunder include such indeterminate number of additional securities as may be issuable to prevent dilution resulting of any stock dividend, stock split, recapitalization or other similar transaction.

(3) Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(c) under the Securities Act, based on the average of the high and low prices of the registrant’s ordinary shares (which will convert into shares of Class A Common Stock of the registrant upon the closing of the registrant’s previously announced initial business combination) as reported on May 20, 2021, which was approximately $10.18 per share.

(4) Previously paid.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

In connection with the proposed business combination (the “Business Combination”) between Andina Acquisition Corp III, a Cayman Islands exempted company (“Andina”, and its successor after it redomiciles as and becomes a Delaware corporation in connection with the Business Combination, the “Company”), and Stryve Foods, LLC, a Texas limited liability company (“Stryve”), pursuant to that certain business combination agreement, dated as of January 28, 2021 (as it may be amended, the “Business Combination Agreement”), by and among, Andina, Andina Holdings LLC, a Delaware limited liability company (“Holdings”), Stryve, Stryve Foods Holdings, LLC, a Texas limited liability company (the “Seller”), and certain other parties named therein, Andina and Stryve entered into subscription agreements with certain investors (the “Closing PIPE Investors”) for the sales of an aggregate of 4,250,000 shares (the “Closing PIPE Shares”) of Class A common stock, par value $0.0001 per share, of the Company (the “Class A Common Stock”), for an aggregate purchase price of $42,500,000 in a private placement in Andina to be consummated simultaneously with the closing of the Business Combination (the “Closing PIPE Investment”). In addition, in connection with the execution of the Business Combination Agreement, (i) Stryve also entered into note purchase agreements with certain investors (the “Bridge Investors” and, together with the Closing PIPE Investors, the “PIPE Investors”) in a private placement for an aggregate of $10,600,000 in unsecured promissory notes of Stryve (the “Bridge Notes”) which were funded by the Bridge Investors and issued upon execution (including certain Stryve’s obligations under certain promissory notes issued by Stryve prior to the execution of the Business Combination Agreement (“Pre-Bridge Notes”) that were exchanged for Bridge Notes), and (ii) Andina and Stryve entered into subscription agreements with the Bridge Investors (in the same form as with the Closing PIPE Investors), where the obligations of Stryve under such Bridge Notes will be used to offset and satisfy the obligations of the Bridge Investors under such subscription agreements at the closing of the Business Combination, whereupon the Bridge Investors (including holders of Pre-Bridge Notes that were exchanged for Bridge Notes) will be issued an aggregate of up to 1,359,398 shares of Class A Common Stock (the “Bridge PIPE Shares” and, together with the Closing PIPE Shares, the “PIPE Shares”) at a twenty percent (20%) discount to the Closing PIPE Shares (the “Bridge PIPE Investment” and, together with the Closing PIPE Investment, the “PIPE Investment”).

This registration statement registers the resale of up to 5,609,398 PIPE Shares to be issued to the PIPE Investors in the PIPE Investment to be consummated simultaneously with the closing of the Business Combination. The PIPE Shares will not be issued and outstanding at the time of the extraordinary general meeting of Andina’s shareholders (the “Special Meeting”) to be held to approve the Business Combination and other proposals. In the event the Business Combination is not approved by Andina shareholders or the other conditions precedent to the consummation of the Business Combination are not met, then the PIPE Shares will not be issued and Andina will seek to withdraw the registration statement prior to its effectiveness.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 15, 2021

PRELIMINARY PROSPECTUS

ANDINA ACQUISITION CORP. III

Up to 5,609,398 Shares of Class A Common Stock

This prospectus relates to the resale from time to time by the selling stockholders named in this prospectus or their permitted transferees (collectively, the “Selling Stockholders”) of up to 5,609,398 shares of Class A common stock (the “PIPE Shares”), par value $0.0001 per share (“Class A Common Stock”), of Andina Acquisition Corp. III, a Cayman Islands exempted company (“Andina”, and its successor after it redomiciles as and becomes a Delaware corporation in connection with the Business Combination (as defined below), the “Company”), which are expected to be issued in a private placement pursuant to the terms of the Subscription Agreements (as defined below) in connection with the Business Combination. If the Business Combination is not consummated, the shares of Class A Common Stock registered pursuant to this prospectus will not be issued.

On January 28, 2021, Andina entered into a Business Combination Agreement (the “Business Combination Agreement”) with Andina Holdings LLC, a Delaware limited liability company (“Holdings”) and a wholly-owned subsidiary of Andina, B. Luke Weil, in the capacity from and after the closing of the transactions contemplated by the Business Combination Agreement (the “Closing”) as the representative for the shareholders of Andina (other than the Seller), Stryve Foods, LLC, a Texas limited liability company (“Stryve”), Stryve Foods Holdings, LLC, a Texas limited liability company (the “Seller”), and R. Alex Hawkins, in the capacity from and after the Closing as the representative for the members of the Seller. Pursuant to the Business Combination Agreement, subject to the terms and conditions set forth therein, (i) promptly after the execution and delivery of the Business Combination Agreement, the Seller and Stryve conducted a reorganization via merger pursuant to which the Seller became a holding company for Stryve, the former owners of Stryve became the owners of the Seller, and the former holders of convertible notes of Stryve became holders of convertible notes of the Seller, and pursuant to which Stryve retained all of its subsidiaries, business, assets and liabilities, and became a wholly-owned subsidiary of the Seller, (ii) prior to the Closing, Andina will be transferred by way of continuation out of the Cayman Islands and domesticated as a corporation in the State of Delaware, (iii) at the Closing, the Seller will contribute to Holdings all of the issued and outstanding equity interests of Stryve in exchange for newly issued non-voting Class B membership interests of Holdings and voting (but non-economic) Class V common stock of Andina, and (iv) Andina will contribute all of its cash and cash equivalents to Holdings, after payment of Andina shareholders that elect to have their Andina shares redeemed or converted in connection with the Closing and Andina’s expenses and other liabilities due at the Closing, in exchange for newly issued voting Class A membership interests of Holdings. Andina will change its name to “Stryve Foods, Inc.” upon consummation of the Business Combination.

Simultaneously with the execution of the Business Combination Agreement, Andina and Stryve entered into subscription agreements with investors (the “Closing PIPE Investors”) for an aggregate of $42,500,000 for 4,250,000 shares of Class A Common Stock of Andina (the “Closing PIPE Shares”) at a price of $10.00 per share in a private placement in Andina (the “Closing PIPE Investment”) to be consummated simultaneously with the Closing. In addition, simultaneously with the Business Combination Agreement, (i) Stryve issued to investors (the “Bridge Investors”) in a private placement $10,600,000 in unsecured promissory notes (the “Bridge Notes”) and (ii) Andina and Stryve entered into subscription agreements with the Bridge Investors (in the same form as with the Closing PIPE Investors), where the obligations of Stryve under such Bridge Notes will be used to offset and satisfy the obligations of the Bridge Investors under such subscription agreements at the Closing, whereupon the Bridge Investors will be issued an aggregate of up to 1,359,398 shares of Class A Common Stock (the “Bridge Shares”) at a twenty percent (20%) discount to the Closing PIPE Shares.

The Selling Stockholders may offer, sell or distribute all or a portion of the shares of Class A Common Stock registered hereby publicly or through private transactions at prevailing market prices or at negotiated prices. We will pay certain offering fees and expenses and fees in connection with the registration of the PIPE Shares and will not receive proceeds from the sale of the PIPE Shares by the Selling Stockholders. Andina’s units, ordinary shares, and warrants are currently listed on the Nasdaq Capital Market and trades under the symbols “ANDAU,” “ANDA,” “ANDAW,” respectively. Upon the consummation of the Business Combination, the Class A Common Stock and warrants of the Company are expected trade on the Nasdaq Stock Market under the symbol “SNAX” and “SNAXW,” respectively.

We are an “emerging growth company” under applicable federal securities laws and will be subject to reduced public company reporting requirements.

INVESTING IN OUR SECURITIES INVOLVES RISKS THAT ARE DESCRIBED IN THE “RISK FACTORS” SECTION BEGINNING ON PAGE 16 OF THIS PROSPECTUS.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is June 15, 2021.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

For investors outside the United States: We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

| i |

FREQUENTLY USED TERMS

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “our,” and “Andina” refer to Andina Acquisition Corp. III, a Delaware corporation, and the term “Combined Company” refers to the company following the consummation of the Business Combination. In this prospectus:

“Amended Holdings Operating Agreement” means the Amended and Restated Operating Agreement of Holdings which will take effect simultaneously with the Business Combination, in the form included as Exhibit 10.16 to this prospectus.

“Andina Board” means the board of directors of Andina.

“Andina common stock” means the shares of common stock, par value $0.0001 per share, of Andina following the Domestication, which shares will have the rights and preferences, and otherwise be subject to the terms and conditions set forth in, the Interim Charter.

“Andina Representative” means B. Luke Weil, in his capacity as the representative from and after the Closing for the shareholders of Andina (other than the Seller and its successor and assignees) pursuant to the Business Combination Agreement.

“Andina Securities” means the Units, the Ordinary Shares, the Rights and the Warrants (and after the Domestication, the Andina common stock and, after the Business Combination, the Class A Common Stock and the Class V Common Stock), collectively.

“Bridge Investors” means the investors in a private placement (the “Bridge PIPE Investment”) for an aggregate of Ten Million Six Hundred Thousand U.S. Dollars ($10,600,000) in consideration of unsecured promissory notes (the “Bridge Notes”) of Stryve funded by the Bridge Investors on the date of the Business Combination Agreement (including certain Stryve obligations under Pre-Bridge Notes that were exchanged for Bridge Notes) that have entered into subscription agreements with Andina pursuant to which the obligations of Stryve under the Bridge Notes will be used to offset and satisfy the Bridge Investors under such subscription agreements at the Closing and the Bridge Investors will be issued shares of Class A Common Stock (the “Bridge PIPE Shares”) at a twenty percent (20%) discount to the Closing PIPE Shares.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated effective as of January 28, 2021, by and among Andina, Andina Holdings LLC, a Delaware limited liability company and a wholly-owned subsidiary of Andina, B. Luke Weil, in the capacity from and after the closing of the transactions contemplated by the Business Combination Agreement as the representative for certain shareholders of Andina, Stryve Foods, LLC, a Texas limited liability company, Stryve Foods Holdings, LLC, a Texas limited liability company, and R. Alex Hawkins, in the capacity from and after the Closing as the representative for the members of the Stryve Foods Holdings, LLC, as it may be amended and supplemented from time to time. A copy of the Business Combination Agreement is included as Exhibit 2.1 to this prospectus.

“Bylaws” means the bylaws of the Company to take effect upon the Domestication, in the form included as Exhibit 3.4 to this prospectus.

“Cayman Islands Companies Act” refers to the Cayman Islands Companies Act (As Revised).

“Class A Common Stock” means the shares of Class A common stock, par value $0.0001 per share, of Andina following the Business Combination, which shares will have full economic and voting rights, and otherwise be subject to the terms and conditions set forth in the Proposed Charter.

“Class V Common Stock” means the shares of Class V common stock, par value $0.0001 per share, of Andina following the consummation of the Business Combination, which shares will have one vote per share, but no economic rights, not be transferrable except in conjunction with the transfer of an equal number of Holdings Class B Units and otherwise be subject to the terms and conditions set forth in the Proposed Charter.

| ii |

“Closing” means the closing of the Business Combination.

“Closing PIPE Investment” means the expected issuance and sale to investors (the “Closing PIPE Investors”) for an aggregate of Forty-Two Million Five Hundred Thousand U.S. Dollars ($42,500,000) of 4,250,000 shares of Class A Common Stock (the “Closing PIPE Shares”) at a price of $10.00 per share in a private placement in Andina pursuant to Subscription Agreements.

“Code” means the Internal Revenue Code of 1986, as amended.

“Company” refers to the combined company immediately following the Business Combination that shall be renamed “Stryve Foods, Inc.” upon the Closing.

“Company Board” means the board of directors of the Company subsequent to the completion of the Business Combination.

“Company Shares” means, collectively, all shares of the Class A common stock and Class V common stock of the Company.

“Current Charter” means Andina’s current Amended and Restated Memorandum and Articles of Association, as may hereafter be amended.

“DGCL” means the Delaware General Corporation Law, as amended.

“Domestication” means the transfer by way of continuation of Andina out of the Cayman Islands, and into the State of Delaware as a Delaware corporation, with the Ordinary Shares of Andina becoming shares of common stock of Andina, as a Delaware corporation, under the applicable provisions of the Cayman Islands Companies Act and the DGCL; the term includes all matters and necessary or ancillary changes in order to effect such Domestication, including the adoption of the Interim Charter (included as Exhibit 3.2 to this prospectus) and the adoption by the Andina Board of the Bylaws (included as Exhibit 3.4 to this prospectus) consistent with the DGCL and changing the name and registered office of Andina.

“DTC” means The Depository Trust Company.

“DWAC” means The Depository Trust Company’s deposit/withdrawal at custodian system.

“Early Termination Event” means the events specified in the Tax Receivables Agreement, which generally includes a voluntary termination of the Tax Receivables Agreement by Andina, or a change in control of Andina

“Employment Agreements” mean the employment agreements required to be delivered at the Closing of the Business Combination.

“Escrow Agreement” means the agreement among the Seller Representative, the Andina Representative and the Escrow Agent, effective as of the Closing of the Business Combination.

“Escrow Agent” means Continental Stock Transfer & Trust Company, or if Continental Stock Transfer & Trust Company is unable or unwilling to serve, another escrow agent reasonably acceptable to the Seller Representative and the Andina Representative.

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“Exchange Agreement” means an agreement to be entered to prior to the Closing between Andina, Holdings and the Seller permitting, among other things, holders of Holdings Class B Units and Class V Common Stock to exchange a set of one Holdings Class B Unit and one share of Class V Common Stock for one share of Class A Common Stock in the form included as Exhibit 10.14 to this prospectus.

| iii |

“GAAP” means U.S. generally accepted accounting principles.

“Holdings” means Andina Holdings LLC, a Delaware limited liability company and wholly owned subsidiary of Andina.

“Holdings Class A Units” means the Class A Common Units of Holdings, which will have full economic and voting rights, and shall otherwise be subject to the terms and conditions set forth in the Amended Holdings Operating Agreement.

“Holdings Class B Units” means the Class B Common Units of Holdings, which will have full economic rights, but no voting rights to the fullest extent permitted by the DCGL, not be transferrable except in conjunction with the transfer of an equal number of shares of Class V Common Stock and shall otherwise be subject to the terms and conditions set forth in the Amended Holdings Operating Agreement.

“Holdings Units” means the Holdings Class A Units and the Holdings Class B Units, collectively.

“Incentive Plan” means the 2021 Omnibus Incentive Plan, a copy of which is included as Exhibit 10.13 to this prospectus.

“initial shareholders” means all of Andina’s shareholders immediately prior to its IPO, including its officers and directors and the underwriters in its IPO to the extent they hold such shares.

“Insiders” means B. Luke Weil and each transferee of Insider Shares.

“Insider Escrow Agreement” means the Share Escrow Agreement, dated as of January 28, 2019, among Andina, the Insiders and the Transfer Agent, which was amended simultaneously with the execution of the Business Combination Agreement to acknowledge the replacement of the Insider Shares held in escrow thereunder with Andina common stock in the Domestication and, in order to match the lock-up period in the Lock-Up Agreement, to extend the lock-up period for their Insider Shares (including any that are transferred to other persons in support of the Transactions) effective as of the Closing so that the testing for the early release with respect to 50% of their Insider Shares will only begin twenty (20) trading days prior to the six (6) month anniversary of the Closing.

“Insider Escrow Account” means the escrow account in which Insider Shares are held in escrow in accordance with the terms of the Insider Escrow Agreement.

“Insider Forfeiture Agreement” means the letter agreement, dated as of January 28, 2021, between each of the Insiders, Andina and the Seller pursuant to which each Insider has agreed to, among other things, cancel certain Insider Shares, Private Rights and Private Warrants held by such Insider, effective as of the Closing, to amend the Insider Escrow Agreement pursuant to which Insider Shares are held in escrow and to extend the lock-up period for their Insider Shares.

“Insider Letter Agreement” means the letter agreement between Andina and each of the Insiders which contains provisions relating to transfer restrictions of the Insider Shares, Private Warrants and Private Rights, indemnification of the Trust Account, waiver of redemption rights and participation in liquidation distributions from the Trust Account.

“Insider Registration Rights Agreement” means the Registration Rights Agreement, dated as of January 28, 2019, by and among Andina and the Insiders, as amended from time to time in accordance with its terms, and as shall be amended in connection with the Business Combination in accordance with the terms of the Business Combination Agreement.

“Insider Shares” means an aggregate of 2,700,000 Ordinary Shares which were originally issued to B. Luke Weil as “Insider Shares” (described in the IPO Prospectus) prior to the IPO.

| iv |

“Interim Charter” means the certificate of incorporation included as Exhibit 3.2 to this prospectus and to be adopted upon the Domestication taking effect.

“Intended Tax Treatment” means the intended tax treatment of the parties to the Business Combination Agreement that the Contribution qualify as tax-deferred exchanges described in Section 721 of the Code (as defined herein), Section 351 of the Code and/or otherwise.

“IPO” means Andina’s initial public offering of its units, Ordinary Shares, rights and warrants pursuant to the IPO Prospectus.

“IPO Prospectus” means the final prospectus of Andina, dated as of January 28, 2019, and filed with the SEC on January 29, 2019 (File No. 333-228530).

“January 2021 Extension” means the extension of the date by which Andina had to complete a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses from January 31, 2021 to April 30, 2021 (or July 31, 2021, if Andina had executed a definitive agreement for such a business combination by April 30, 2021), as approved by the Andina shareholders at a special meeting held on January 27, 2021.

“July 2020 Extension” means the extension of the date by which Andina had to complete a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses from July 31, 2020 to October 31, 2020 (or December 31, 2020, if Andina had executed a definitive agreement for such a business combination by October 31, 2020), as approved by the Andina shareholders at a special meeting held on July 29, 2020.

“Lock-Up Agreement” means the agreement between the Seller, Andina and the Andina Representative entered into simultaneously with the Business Combination Agreement with respect to the Seller Consideration Units and shares of Class V Common Stock received by Seller in the Transactions, including the Escrow Securities, any additional securities issued by Andina after the Closing pursuant to the post-Closing consideration adjustments under the Business Combination Agreement and certain additional shares that may be issued after the Closing.

“Minimum Cash Condition” means the condition, which may be waived by Stryve, to Stryve’s obligations under the Business Combination Agreement that, upon the Closing, after giving effect to completion of the Business Combination and payment of redemptions, if any, Andina shall have cash or cash equivalents equal to at least $19,000,000, less certain proceeds received by Stryve from Bridge Notes (including as a result of satisfaction or offset).

“Nasdaq” means the Nasdaq Capital Market.

“Non-Compete Agreements” means the Non-Competition and Non-Solicitation Agreements between the Seller and certain significant members of the Seller entered into simultaneously with the Business Combination Agreement.

“October 2020 Extension” means the extension of the date by which Andina had to complete a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses from October 31, 2020 to January 31, 2021 (or April 30, 2021, if Andina had executed a definitive agreement for such a business combination by January 31, 2021) approved by the Andina shareholders at a special meeting held on October 28, 2020.

“Organizational Documents” means, with respect to any Person that is an entity, its certificate of incorporation or formation, bylaws, operating agreement, memorandum and articles of association or similar organizational documents, in each case, as amended.

“Ordinary Shares” means the ordinary shares, par value $.0001 per share, of Andina prior to the Domestication.

“PFIC” means a passive foreign investment company.

| v |

“PIPE Investors” means the investors in the Bridge PIPE Investment and the Closing PIPE Investment.

“PIPE Investment” means the Bridge PIPE Investment and the Closing PIPE Investment.

“Pre-Bridge Notes” means the Convertible Promissory Notes issued by the Seller pursuant to the Convertible Note Purchase Agreements entered into after January 1, 2021 (including those entered into during the period between signing the Business Combination Agreement and the Business Combination).

“Private Rights” means the right included as part of each Private Unit, entitling the holder thereof to receive one-tenth (1/10) of an Ordinary Share upon consummation of Andina’s initial business combination.

“Private Securities” means, collectively, Private Units and their component Ordinary Shares, Private Rights and Private Warrants, together with all Ordinary Shares issuable pursuant to Private Rights and Ordinary Shares issuable upon exercise of Private Warrants (and, after Domestication, all of the Andina common stock, Andina warrants, Andina rights into which any of the foregoing shall be converted, or which may be issuable pursuant to or upon exercise of any of the foregoing).

“Private Units” means the units issued by Andina in a private placement to the Insiders at the time of the consummation of the IPO consisting of one (1) Ordinary Share, one (1) Private Right and one (1) Private Warrant.

“Private Warrants” means one whole warrant that was included in as part of each Private Unit, entitling the holder thereof to purchase one (1) Ordinary Share at a purchase price of $11.50 per share.

“Proposed Charter” means the first amended and restated certificate of incorporation in the form included as Exhibit 3.3 to this prospectus, proposed to be in effective at and following the Closing of the Business Combination,.

“Public Rights” means the right that was included as part of each Public Unit, entitling the holder thereof to receive one-tenth (1/10) of an Ordinary Share upon consummation of Andina’s initial merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses.

“Public Shareholders” means the holders of Andina Public Shares.

“Public Shares” means the Ordinary Shares sold in Andina’s initial public offering (including overallotment units acquired by Andina’s underwriters), whether they were purchased in the IPO or thereafter in the open market.

“Public Shareholder” means a holder of Public Shares as of the relevant date.

“Public Securities” means, collectively, all of the Public Units, all of the Ordinary Shares, Public Warrants and Public Rights (while such securities are components of Public Units and as separate securities), together with all Ordinary Shares issuable pursuant to Public Rights and Ordinary Shares issuable upon exercise of Public Warrants (and, after Domestication, all of the Andina common stock, warrants and rights into which any of the foregoing may be converted, or which may be issuable pursuant to or upon exercise of any of the foregoing).

“Pubic Units” means all of the issued and outstanding Units which are not Private Units.

“Public Warrant” means one whole warrant that was included in as part of each Public Unit, entitling the holder thereof to purchase one (1) Ordinary Share at a purchase price of $11.50 per share.

“Public Warrant Holders” means the holders of the Public Warrants.

“Redemption” means a redemption of Public Shares for the Redemption Price.

“Redemption Date” means that date on which holders of Public Shares may be eligible to redeem their Public Shares for Redemption in accordance with the Current Charter.

| vi |

“Redemption Price” means an amount equal to a pro rata portion of the aggregate amount then on deposit in the Trust Account calculated in accordance with the Current Charter as of the applicable Redemption Date.

“Registration Rights Agreement” means the Registration Rights Agreement between the Seller and Andina entered into simultaneously with the Business Combination Agreement.

“Reorganization” means the reorganization of the Seller and Stryve via a merger pursuant to the Texas Business Organizations Code, as amended, pursuant to the Business Combination Agreement.

“Rights” means Private Rights and Public Rights, collectively.

“Rights Agreement” means the Rights Agreement between Andina and Continental Stock Transfer & Trust Company, in its capacity as Right Agent.

“SEC” means the United States Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Seller” means Stryve Foods Holdings, LLC, a Texas limited liability company.

“Seller Consideration Units” means the non-voting Class B Membership Interests of Holdings issued to the Seller at the Closing pursuant to the Business Combination Agreement.

“Seller Representative” means R. Alex Hawkins, in the capacity as the representative from and after the Closing for the members of the Seller after giving effect to the Reorganization in accordance with the terms of the Business Combination Agreement.

“Special Meeting” means the extraordinary general meeting of Andina, and any adjournments thereof.

“Stryve” means Stryve Foods, LLC, a Texas limited liability company.

“Subscription Agreements” means the Subscription Agreements, entered into simultaneously with the Business Combination Agreement, between Andina and each of the PIPE Investors (including the Closing PIPE Investors and the Bridge PIPE Investors) for the PIPE Investment.

“Target Company” means each of Stryve and its direct and indirect subsidiaries.

“Tax Group” means Andina and its applicable consolidated unitary or combined subsidiaries.

“Tax Receivables Agreement” means the Tax Receivables Agreement to be entered into between Andina and the Seller prior to the closing of the Business Combination in the form included as Exhibit 10.15 to this prospectus.

“TRA Holder” means a holder of a set of a Holdings Class B Unit and a share of Class V Common Stock.

“TRA Holder Representative” means the representative appointed by the Seller (or its successors or assigns) under the Tax Receivables Agreement.

“Transfer Agent” means Continental Stock Transfer & Trust Company.

“Trust” or “Trust Account” means the trust account established by Andina with the proceeds from the IPO pursuant to the Trust Agreement in accordance with the IPO Prospectus.

“Trust Agreement” means the Investment Management Trust Agreement, dated as of January 28, 2019, as it may be amended, by and between Andina and the Trustee, as well as any other agreements entered into related to or governing the Trust Account.

| vii |

“Trustee” means Continental Stock Transfer & Trust Company, in its capacity as trustee under the Trust Agreement.

“Units” means units, each consisting of one ordinary share, one warrant and one right, issued by Andina pursuant to, and with the terms set forth in, the Current Charter.

“Up-C” means the umbrella partnership C-corporation structure into which the combination company after the Business Combination will be organized.

“U.S. Holder” means a beneficial owner of Ordinary Shares that is for U.S. federal income tax purposes: (a) an individual citizen or resident of the United States; (b) a corporation (or other entity treated as a corporation) that is created or organized (or treated as created or organized) in or under the laws of the United States, any state thereof or the District of Columbia; (c) an estate whose income is includible in gross income for U.S. federal income tax purposes regardless of its source; or (d) a trust if (i) a U.S. court can exercise primary supervision over the trust’s administration and one or more U.S. persons are authorized to control all substantial decisions of the trust, or (ii) it has a valid election in effect under applicable U.S. Treasury Regulations to be treated as a U.S. person

“Warrants” means Private Warrants and Public Warrants, collectively.

“Warrant Agent” means Continental Stock Transfer & Trust Company, in its capacity as warrant agent under the Warrant Agreement.

“Warrant Agreement” means the Warrant Agreement, dated as of January 28, 2019, between Andina and the Warrant Agent, which governs Andina’s outstanding Warrants.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. These forward-looking statements include, among other things, statements about the parties’ ability to close the Business Combination, the timing of the closing of the Business Combination, the anticipated benefits of the Business Combination, the financial conditions, results of operations, earnings outlook and prospects of Andina, Stryve and the post-combination Company and the period following the consummation of the Business Combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would,” “will,” “seek,” “target,” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements are based on information available as of the date of this prospectus and on the current expectations, forecasts and assumptions of the management of Andina and Stryve, involve a number of judgments, risks and uncertainties and are inherently subject to changes in circumstances and their potential effects and speak only as of the date of such statements. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed, contemplated or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” those discussed and identified in public filings made with the SEC by Andina and the following:

| ● | expectations regarding (and Stryve’s ability to meet expectations regarding) Stryve’s strategies and future financial performance, including Stryve’s future business plans or objectives, anticipated demand and acceptance of its products, pricing, marketing plans, manufacturing, production and supply capabilities, operating expenses, market trends, revenues, liquidity, cash flows and uses of cash, capital expenditures, and Stryve’s ability to invest in growth initiatives; |

| viii |

| ● | Stryve has a history of losses and may be unable to achieve or sustain profitability; | |

| ● | Stryve may not be able to compete successfully in the highly competitive snacking and nutritional snacking industry; | |

| ● | Stryve’s brand and reputation may be diminished due to real or perceived quality or health issues with its products, including meat, which could materially and adversely affect its business, financial condition and results of operations; | |

| ● | Most of Stryve’s products are manufactured in its single facility in Oklahoma and any damage to or disruption at this facility would materially and adversely affect its business, financial condition and results of operations; | |

| ● | The loss of Stryve’s USDA grant of approval from its Oklahoma facility would materially adversely impact its business, results of operations and financial condition; | |

| ● | the occurrence of any event, change or other circumstances that could delay the Business Combination or give rise to the termination of the Business Combination Agreement; | |

| ● | the outcome of any legal proceedings that may be instituted against Andina, Stryve and others following announcement of the Business Combination Agreement and the transactions contemplated therein; | |

| ● | the inability to complete the Business Combination due to the failure to obtain Andina shareholders’ approval or satisfy other conditions to closing under the Business Combination Agreement; | |

| ● | the risk that the proposed Business Combination disrupts current plans and operations of Stryve as a result of the announcement and consummation of the Business Combination; | |

| ● | the ability to recognize the anticipated benefits of the Business Combination; | |

| ● | unexpected costs related to the proposed Business Combination; | |

| ● | the amount of any redemptions by shareholders of Andina being greater than expected; | |

| ● | the management and board composition of the Company following the proposed Business Combination; | |

| ● | the ability to list the Company’s securities on Nasdaq; | |

| ● | limited liquidity and trading of the Company’s securities; | |

| ● | geopolitical risk and changes in applicable laws or regulations; | |

| ● | the possibility that Andina or Stryve or the Company may be adversely affected by other economic, business, and/or competitive factors; | |

| ● | the possibility that the COVID-19 pandemic, or another major disease or epidemic, disrupts Stryve’s business; | |

| ● | litigation and regulatory enforcement risks, including the diversion of management time and attention and the additional costs and demands on Stryve’s resources; and | |

| ● | risks that the consummation of the Business Combination is substantially delayed or does not occur, impacting the ability of Stryve to operate or implement its business plan. |

Should one or more of these risks or uncertainties materialize, or should any of the assumptions made by the management of Andina or Stryve prove incorrect, actual results may vary in material respects from those projected in or contemplated by these forward-looking statements.

All subsequent written and oral forward-looking statements concerning the Business Combination or other matters addressed in this prospectus and attributable to Andina or Stryve or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this prospectus. Except to the extent required by applicable law or regulation, neither Andina nor Stryve undertakes any obligation to update these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events.

| ix |

SUMMARY OF THE PROSPECTUS

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Andina’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Stryve’s Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements included elsewhere in this prospectus.

Parties to the Business Combination

Andina

Andina is a blank check company incorporated as a Cayman Islands exempted company on July 29, 2016, for the purpose of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses.

Andina’s units, Ordinary Shares, rights and warrants are currently listed on Nasdaq under the symbols “ANDAU,” “ANDA,” “ANDAR” and “ANDAW,” respectively. Andina’s units, each consisting of one ordinary share, one warrant and one right, will automatically separate into their component securities upon consummation of the Business Combination and, as a result, will no longer exist as a separate security. Upon the closing of the Business Combination, each holder of a right will receive one-tenth (1/10) of one share of Class A Common Stock of the Company. Upon the Closing, Andina intends to change its name from “Andina Acquisition Corp. III” to “Stryve Foods, Inc.” Andina intends to apply to continue the listing of its Class A common stock and warrants on Nasdaq under the symbols “SNAX” and “SNAXW,” respectively, upon the Closing.

Andina’s principal executive offices are located at Calle 113 # 7-45 Torre B, Oficina 1012, Bogotá, Colombia and its phone number is (646) 565-3861.

Holdings

Andina Holdings LLC (“Holdings”) is a Delaware limited liability company and wholly owned subsidiary of Andina.

Andina Representative

B. Luke Weil (the “Andina Representative”) is serving as the Andina Representative under the Business Combination Agreement, and in such capacity will represent the interests of Andina’s shareholders after the Closing (other than the Seller) with respect to certain matters under the Business Combination Agreement.

| 1 |

Stryve

Stryve Foods, LLC is a Texas limited liability company (“Stryve”) formed on January 13, 2017.

Stryve is an emerging healthy snacking company which manufactures, markets and sells highly differentiated healthy snacking products that Stryve believes can disrupt traditional snacking categories. Stryve’s mission is “to help Americans snack better and live happier, better lives.” Stryve offers convenient snacks that are lower in sugar and carbohydrates and higher in protein than other snacks. Stryve offers all-natural, delicious snacks which it believes are nutritious and offer consumers a convenient healthy snacking option for their on-the-go lives.

Stryve’s current product portfolio consists primarily of air-dried meat snack products marketed under the Stryve®, Kalahari®, Braaitime®, and Vacadillos® brand names. Biltong is a process for preserving meat through air drying that originated centuries ago in South Africa. Unlike beef jerky, Stryve’s all-natural air-dried meat snack products are made of beef and spices, are never cooked, contain zero grams of sugar, and are free of monosodium glutamate (MSG), gluten, nitrates, nitrites, and preservatives. As a result, Stryve’s products are Keto and Paelo diet friendly. Further, based on protein density and sugar content, Stryve believes that its air-dried meat snack products are some of the healthiest shelf-stable snacks available today.

Stryve’s principal executive offices are located at 5801 Tennyson Parkway, Suite 275, Plano, Texas 75024 and its phone number is (972) 987-5130.

Seller

Stryve Foods Holdings, LLC (“Seller”) is a Texas limited liability company which currently acts as a holding company and sole member of Stryve.

Seller Representative

R. Alex Hawkins (the “Seller Representative”) is serving as the representative from and after the Closing for the members of the Seller after giving effect to the Reorganization in accordance with the terms of the Business Combination Agreement.

The Domestication

Andina and Stryve and the other parties thereto have agreed to the Business Combination under the terms of the Business Combination Agreement. If the Business Combination is to be consummated, prior and as a condition to the Closing, Andina will (a) be transferred by way of continuation out of the Cayman Islands and domesticated as a corporation in the State of Delaware (which is referred to herein as the “Domestication”); (b) in connection therewith, adopt upon the Domestication taking effect, the Interim Charter in place of Andina’s Current Charter which will remove or amend those provisions of Andina’s Current Charter that terminate or otherwise cease to be applicable as a result of the Domestication; and (c) file the Interim Charter with the Secretary of State of Delaware. At the time of the Domestication, simultaneously with the adoption of the Interim Charter, the Andina Board intends to adopt Bylaws. Upon effectiveness of the Domestication, all of Andina’s outstanding securities will convert to outstanding securities of the continuing corporation.

The Business Combination and Business Combination Agreement

Pursuant to the Business Combination Agreement, as described in more detail in the below, (i) promptly after the execution and delivery of the Business Combination Agreement, the Seller and Stryve conducted a reorganization via a merger pursuant to which the Seller became a holding company for Stryve, the former owners of Stryve became the owners of the Seller, and the former holders of convertible notes of Stryve became holders of convertible notes of the Seller, and pursuant to which Stryve retained all of its subsidiaries, business, assets and liabilities, and became a wholly-owned subsidiary of the Seller, (ii) prior to the Closing, Andina will consummate the Domestication, (iii) at the Closing, the Seller will contribute to Holdings all of the issued and outstanding equity interests of Stryve in exchange for newly issued non-voting Class B membership interests of Holdings and voting (but non-economic) Class V Common Stock; (iv) Andina will contribute all of its cash and cash equivalents to Holdings, after payment of Andina shareholders that elect to have their Andina shares redeemed or converted in connection with the Closing and Andina’s expenses and other liabilities due at the Closing, in exchange for newly issued voting Class A membership interests of Holdings (the “Seller Consideration Units”). The Seller Consideration Units will provide the holder with economic rights, but not voting rights, with respect to Holdings and the Class V Common Stock of the Company will provide the holder with voting rights, but not economic rights, with respect to the Company (for more information, see the section in this prospectus entitled “Description of Securities”).

| 2 |

At the Closing, Andina will change its name to “Stryve Foods, Inc.” and the combined company will be organized in an Up-C structure, in which substantially all of the assets of the combined company will be held by Holdings, and Andina’s only assets will be its equity interests in Holdings.

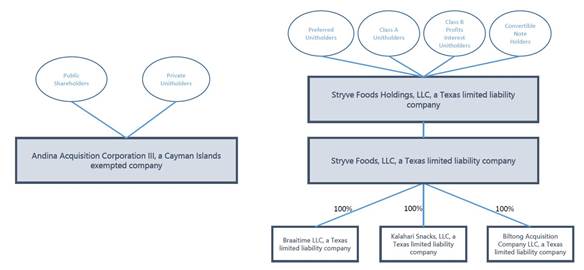

Existing Organizational Structure

The diagrams below depict simplified versions of the current organizational structures of Andina and Stryve, respectively.

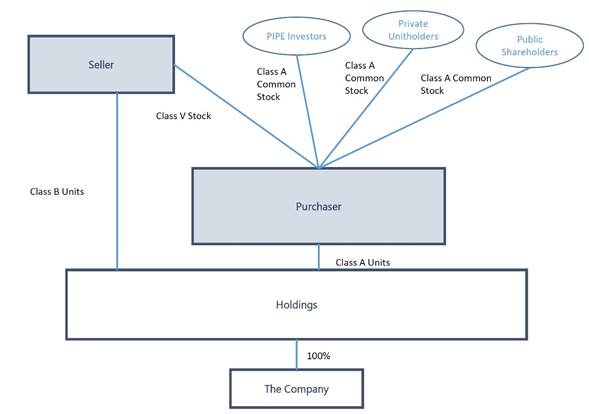

Organizational Structure Following the Business Combination

Following the Closing, the combined company will be organized in an Up-C structure, in which substantially all of the assets of the combined company will be held by Holdings, and Andina’s only assets will be its equity interests in Holdings. The diagram below depicts a simplified version of Andina’s organizational structure immediately following the completion of the Business Combination.

| 3 |

Seller Consideration

Subject to and upon the terms and conditions of the Business Combination Agreement, in exchange for the Seller Contribution, Holdings shall issue to the Seller a number of newly issued Holdings Class B Units, also referred to as Seller Consideration Units, equal in value to (the “Seller Consideration”): (i) One Hundred and Thirty Million U.S. Dollars ($130,000,000), minus (ii) the amount, if any, by which the target consolidated net working capital amount of $553,635.45 exceeds the consolidated net working capital of Stryve (but not less than zero), plus (iii) the amount, if any, by which the consolidated net working capital of Stryve exceeds the target consolidated net working capital amount of $553,635.45 (but not less than zero), minus (iv) the amount of indebtedness of Stryve at the Closing (excluding certain capitalized leases and any obligations under the Bridge Notes or other convertible debt of the Seller that is converted into equity in connection with the Closing), minus (v) the amount of Stryve’s transaction expenses, with each Holdings Class B Unit valued for such purposes at a price of $10.00 per unit. Additionally, Andina will issue to the Seller a number of newly issued shares of Class V Common Stock equal to the number of Seller Consideration Units The Seller may thereafter distribute the Class V Common Stock and Seller Consideration Units to its members.

Subject to and upon the terms and conditions of the Business Combination Agreement, in exchange for the Andina Contribution, Holdings shall issue to Andina a number of newly issued Holdings Class A Units so that after giving effect to such issuance Andina will have a number of Holdings Class A Units equal to the number of issued and outstanding shares of Class A Common Stock as of the Closing (after giving effect to the issuance of any shares in any PIPE Investment and the redemption or conversion of shareholders in the Redemption).

The Seller Consideration Units (and related number of shares of Class V Common Stock) will be issued based on an estimate of Stryve’s consolidated indebtedness, net working capital and transaction expenses as of the Closing and subject to a post-Closing true-up.

| 4 |

The Escrow Units

At the Closing, one percent (1%) of the Seller Consideration Units otherwise issuable by Holdings at the Closing and an equal number of shares of Class V Common Stock otherwise issuable at the Closing (the “Escrow Units”) to the Seller will be deposited into a segregated escrow account with Continental Stock Transfer & Trust Company (or such other escrow agent reasonably acceptable to Andina Representative and Seller Representative), as escrow agent, and held in escrow together with any dividends, distributions or other income on the Escrow Units (the “Escrow Property”) in accordance with an escrow agreement to be entered into in connection with the Transactions (the “Escrow Agreement”). The Escrow Property will be held in the escrow account after the Closing until the parties have reviewed and agreed upon the Closing working capital of Stryve and will be used to serve as the sole source of payment for any purchase price adjustment in favor of Andina. The Seller will have the right to vote the Escrow Units while they are held in escrow.

Representations and Warranties

The Business Combination Agreement contains a number of representations and warranties by each of Andina, Stryve and the Seller. Many of the representations and warranties are qualified by materiality or Material Adverse Effect. “Material Adverse Effect” as used in the Business Combination Agreement means with respect to any specified person or entity, any fact, event, occurrence, change or effect that has had or would reasonably be expected to have, individually or in the aggregate, a material adverse effect on the business, assets, liabilities, results of operations, or condition (financial or otherwise) of such person or entity and its subsidiaries, taken as a whole, or the ability of such person or entity or any of its subsidiaries on a timely basis to consummate the transactions contemplated by the Business Combination Agreement or the ancillary documents to which it is a party or bound or to perform its obligations thereunder, in each case subject to certain customary exceptions. Certain of the representations are subject to specified exceptions and qualifications contained in the Business Combination Agreement or in information provided pursuant to certain disclosure schedules to the Business Combination Agreement.

Closing Conditions

The Closing is subject to the satisfaction of certain closing conditions, including that there not have been a material adverse effect on the business of Stryve and that after giving effect to completion of the Business Combination and payment of the redemption, if any, Andina shall have cash or cash equivalents equal to at least $19,000,000, less certain proceeds received by Stryve from Bridge Notes (including as a result of satisfaction or offset of obligations owed by Stryve under Pre-Bridge Notes that were exchanged for Bridge Notes).

Related Agreements

Registration Rights Agreement

Simultaneously with the execution of the Business Combination Agreement, the Seller entered into a Registration Rights Agreement with Andina (the “Registration Rights Agreement”), which will become effective at the Closing. Under the Registration Rights Agreement, the Seller will hold registration rights that obligate Andina to register for resale under the Securities Act all or any portion of any Exchange Shares issued after the Closing and, solely with respect to a distribution by the Seller to its members, the Seller Consideration Units and shares of Class V Common Stock received by Seller in the Transactions, including the Escrow Securities any additional securities issued by Andina after the Closing pursuant to the post-Closing consideration adjustments under the Business Combination Agreement (collectively, the “Registrable Securities”). Seller (or transferees) holding at least 15% of the Registrable Securities then issued and outstanding will be entitled to make a written demand for registration under the Securities Act of all or part of their Registrable Securities. Subject to certain exceptions, if any time after the Closing, Andina proposes to file a registration statement under the Securities Act with respect to its securities, Andina will be required to give notice tot Seller as to the proposed filing and offer the Seller an opportunity to register the sale of such number of Registrable Securities as requested by the Seller in writing. In addition, subject to certain exceptions, the Seller will be entitled to request in writing that Andina register the resale of any or all of such Registrable Securities on Form S-3 and any similar short-form registration that may be available at such time. Andina also agreed to file within the later of (i) 60 days after the filing of Andina’s 8-K for the Closing and (ii) the date that the registration statement for the PIPE Investors has been declared effective by the SEC, a resale registration statement for the resale of the Registrable Securities and to use its commercially reasonable efforts to cause such registration statement to be declared effective as soon as possible thereafter.

| 5 |

Under the Registration Rights Agreement, Andina agreed to indemnify the Seller and certain persons or entities related to the Seller such as its officers, directors, employees, agents and representatives against any losses or damages resulting from any untrue statement or omission of a material fact in any registration statement or prospectus pursuant to which they sell Registrable Securities, unless such liability arose from their misstatement or omission, and the Seller agreed to indemnify Andina and certain persons or entities related to Andina such as its officers and directors and underwriters against all losses caused by the Seller’ misstatements or omissions in those documents.

Insider Forfeiture Agreement

Simultaneously with the execution of the Business Combination Agreement, B. Luke Weil and certain other Andina shareholders (collectively with B. Luke Weil, the “Insiders”), who received any of the 2,700,000 Andina Ordinary Shares issued to B. Luke Weil as “Insider Shares” prior to Andina’s initial public offering (the “Insider Shares”) each entered into a letter agreement with Andina and the Seller (the “Insider Forfeiture Agreement”), pursuant to which such Insider agreed to cancel, effective as of the Closing, (a) a number of Insider Shares equal to (i) fifty percent (50%) of the Insider Shares held by such Insider as of the date of the Business Combination Agreement, minus (ii) the number of Insider Shares, if any, approved by the Seller in writing for transfer and actually transferred by such Insider to other persons or entities in support of the Transactions, and (b) a number of the warrants and rights purchased by such Insider in the private placement conducted by Andina in connection with its initial public offering equal (collectively, the “Private Warrants and Rights”) to (i) fifty percent (50%) of the Private Warrants and Rights held by such Insider as of the date of the Business Combination Agreement, minus (ii) the number of Private Warrants and Rights, if any, approved by the Seller in writing for transfer and actually transferred by such Insider to other persons or entities in support of the Transactions. Each Insider also agreed to enter into the Share Escrow Amendment, as described below.

PIPE Investment

Simultaneously with the execution of the Business Combination Agreement, Andina and Stryve entered into subscription agreements (each, a “Subscription Agreement”) with certain investors (the “Closing PIPE Investors”) for an aggregate of Forty-Two Million Five Hundred Thousand U.S. Dollars ($42,500,000) for 4,250,000 shares of Class A Common Stock (the “Closing PIPE Shares”) at a price of $10.00 per share in a private placement in Andina to be consummated simultaneously with the closing of the Transactions (the “Closing PIPE Investment”). The consummation of the transactions contemplated by the Subscription Agreement is conditioned on the concurrent Closing and other customary closing conditions. Each Closing PIPE Investor agreed in the Subscription Agreement (and in the PIPE Registration Rights Agreement as well) that it and its affiliates will not have any right, title, interest or claim of any kind in or to any monies in Andina’s Trust Account held for its Public Shareholders, and agreed not to, and waived any right to, make any claim against the Trust Account (including any distributions therefrom).

In addition, simultaneously with the execution of the Business Combination Agreement, (i) Stryve entered into note purchase agreements with certain investors (the “Bridge Investors” and, together with the Closing PIPE Investors, the “PIPE Investors”) in a private placement for an aggregate of Ten Million Six Hundred Thousand U.S. Dollars ($10,600,000) in unsecured promissory notes of Stryve (the “Bridge Notes”) to be funded by the Bridge Investors and issued upon execution (including certain Company obligations under certain promissory notes issued by Stryve prior to the execution of the Business Combination Agreement (“Pre-Bridge Notes”) that were exchanged for Bridge Notes), and (ii) Andina and Stryve entered into Subscription Agreements with the Bridge Investors (in the same form as with the Closing PIPE Investors), where the obligations of Stryve under such Bridge Notes will be used to offset and satisfy the obligations of the Bridge Investors under such Subscription Agreements at the Closing, whereupon the Bridge Investors (including holders of Pre-Bridge Notes that were exchanged for Bridge Notes) will be issued shares of Class A Common Stock (the “Bridge PIPE Shares” and, together with the Closing PIPE Shares, the “PIPE Shares”) at a twenty percent (20%) discount to the Closing PIPE Shares (the “Bridge PIPE Investment” and, together with the Closing PIPE Investment, the “PIPE Investment”).

| 6 |

PIPE Registration Rights Agreement

Simultaneously with the execution and delivery of the Subscription Agreements, Andina entered into a Registration Rights Agreement (the “PIPE Registration Rights Agreement”) with the PIPE Investors pursuant to which Andina agreed to file with the SEC on or prior to the 10th business day after the date on which Andina files the definitive Registration Statement/prospectus for the Special Meeting a registration statement for the resale of the PIPE Shares to be issued to the PIPE Investors (the “Shelf Registration Statement”), and to cause such Shelf Registration Statement to become effective the 60th day following the Closing (or, in the event the SEC notifies Andina that it will review the Shelf Registration Statement, the 120th day following the Closing), subject to liquidated damages of 1% of the subscription price paid by each PIPE Investor per month if it does not timely file such Shelf Registration Statement, meet such registration effectiveness requirement or fails to keep such Shelf Registration Statement effective. The PIPE Registration Rights Agreement prohibits other persons from using piggy-back registration rights with respect to the Shelf Registration Statement and prohibits Andina from filing other registration statements (subject to certain exceptions) until the Shelf Registration Statement is effective.

Under the PIPE Registration Rights Agreement, Andina agreed to indemnify the PIPE Investors and certain persons or entities related to the PIPE Investors against any losses or damages resulting from any untrue statement or omission of a material fact in the Shelf Registration Statement, unless such liability arose from their misstatement or omission, and each PIPE Investor agreed to severally indemnify Andina and certain persons or entities related to Andina against all losses caused by such PIPE Investor’s misstatements or omissions in those documents.

Tax Receivables Agreement

At the Closing of the Business Combination, Andina, Holdings, Seller and the TRA Holder Representative will enter into the Tax Receivables Agreement. Pursuant to the Tax Receivables Agreement, Andina will generally be required to pay the TRA Holders 85% of the amount of savings, if any, in U.S. federal, state, local, and foreign taxes that are based on, or measured with respect to, net income or profits, and any interest related thereto that the Tax Group(i.e., Andina’s and applicable consolidated, unitary, or combined subsidiaries) realizes, or is deemed to realize, as a result of certain tax attributes, which include:

| ● | tax basis adjustments resulting from taxable exchanges of Seller Consideration Units and Class V Common Stock (including any such adjustments resulting from certain payments made by Andina under the Tax Receivables Agreement) acquired by us from a TRA Holder pursuant to the terms of the Amended Holdings Operating Agreement; and | |

| ● | tax deductions in respect of portions of certain payments made under the Tax Receivables Agreement. |

Under the Tax Receivables Agreement, the Tax Group will generally be treated as realizing a tax benefit from the use of a Tax Attribute on a “with and without” basis, thereby generally treating the Tax Attributes as the last item used, subject to several exceptions including without limitation: (i) the carryback of tax items arising from other tax attributes are ignored and will not impact a prior year’s “with and without” calculation, (ii) state and local tax savings are calculated using an assumed tax rate, (iii) the determination of any incremental basis adjustment in respect of payments under the Tax Receivables Agreement is made on an iterative basis continuing until any incremental basis adjustment is immaterial, (iv) as described below in the event that any Tax Attributes initially claimed or utilized by the Tax Group are disallowed, the TRA Holders will not be required to reimburse Andina for any excess payments that may previously have been made, rather any such excess payments made to such TRA Holders will be applied against and reduce any future cash payments otherwise required to be made by Andina under the Tax Receivables Agreement to applicable TRA Holders after the determination of such excess, and (v) upon the occurrence of certain Early Termination Events several assumptions are used in determining the “with and without” calculation as described below.

| 7 |

Payments under the Tax Receivables Agreement generally will be based on the tax reporting positions that Andina determines (with the amount of subject payments determined in consultation with an advisory firm and subject to the TRA Holder Representative’s review and consent), and the IRS or another taxing authority may challenge all or any part of a position taken with respect to Tax Attributes or the utilization thereof, as well as other tax positions that Andina takes, and a court may sustain such a challenge. In the event that any Tax Attributes initially claimed or utilized by the Tax Group are disallowed, the TRA Holders will not be required to reimburse Andina for any excess payments that may previously have been made pursuant to the Tax Receivables Agreement, for example, due to adjustments resulting from examinations by taxing authorities. Rather, any excess payments made to such TRA Holders will be applied against and reduce any future cash payments otherwise required to be made by Andina under the Tax Receivables Agreement after the determination of such excess. However, a challenge to any Tax Attributes initially claimed or utilized by the Tax Group may not arise for a number of years following the initial time of such payment and, even if challenged earlier, such excess cash payment may be greater than the amount of future cash payments that Andina might otherwise be required to make under the terms of the Tax Receivables Agreement and, as a result, there might not be future cash payments against which such excess can be applied. As a result, in certain circumstances Andina could be required to make payments under the Tax Receivables Agreement in excess of the Tax Group’s actual savings in respect of the Tax Attributes, which could materially impair the financial condition of Andina and the Tax Group.

The Tax Receivables Agreement will provide that, in the event of certain Early Termination Events, Andina will be required to make a lump-sum cash payment to all the TRA Holders equal to the present value of all forecasted future payments that would have otherwise been made under the Tax Receivables Agreement, which lump-sum payment would be based on certain assumptions, including those relating to there being sufficient future taxable income of the Tax Group to fully utilize the Tax Attributes over certain specified time periods and that all TRA Holders that had not yet exchanged units for Class A Common Stock are deemed exchanged for cash. The lump-sum payment could be material and could materially exceed any actual tax benefits that the Tax Group realizes subsequent to such payment.

As a result of the foregoing, in some circumstances (i) Andina could be required to make payments under the Tax Receivables Agreement that are greater than or less than the actual tax savings that the Tax Group realizes in respect of the Tax Attributes and (ii) it is possible that Andina may be required to make payments years in advance of the actual realization of tax benefits (if any, and may never actually realize the benefits paid for) in respect of the Tax Attributes (including if any Early Termination Events occur). In these situations, Andina’s obligations under the Tax Receivables Agreement could have a material and adverse impact on Andina’s liquidity and could have the effect of delaying, deferring, or preventing certain mergers, asset sales, other forms of business combinations or other changes of control. There can be no assurance that Andina will be able to finance its obligations under the Tax Receivables Agreement in a manner that does not adversely affect its working capital and growth requirements.

Andina will be required to notify and keep the TRA Holder Representative reasonably informed regarding tax audits or other proceedings the outcome of which is reasonably expected to reduce or defer payments to any TRA Holder under the Tax Receivables Agreement and the TRA Holder Representative and any affected TRA Holder has the right to discuss with Andina, and provide input and comment to Andina regarding, any portion of any such tax audit or proceeding. Andina will not be permitted to settle or fail to contest any issue pertaining to income taxes that is reasonably expected to materially and adversely affect the TRA Holders’ rights and obligations under the Tax Receivables Agreement without the consent of the TRA Holder Representative (which is not to be unreasonably withheld or delayed).

Under the Tax Receivables Agreement, Andina will be required to provide the TRA Holder Representative with a schedule showing the calculation of payments that are due under the Tax Receivables Agreement with respect to each taxable year. This calculation will be based upon the advice of our tax advisors and an advisory firm. Payments under the Tax Receivables Agreement will generally be required to be made to the TRA Holders a short period of time after this schedule becomes final pursuant to the procedures set forth in the Tax Receivables Agreement, although interest on such payments will begin to accrue at from the due date (without extensions) of the U.S. federal income tax return of Andina. Any late payments that may be made under the Tax Receivables Agreement will continue to accrue interest (generally at a default rate) until such payments are made.

| 8 |

Risk Factors

You should consider all the information contained in this prospectus before making a decision to invest in our Class A common stock. In particular, you should consider the risk factors described under “Risk Factors” beginning on page 16. Such risks include, but are not limited to, the following risks with respect to the Company subsequent to the Business Combination:

Risks Related to Stryve’s Business, Brand, Products and Industry

| ● | Stryve has a history of losses and may be unable to achieve or sustain profitability. | |

| ● | Pandemics, epidemics or disease outbreaks, such as the novel coronavirus (“COVID-19”), may disrupt Stryve’s business, including, among other things, consumption and trade patterns, supply chain, and production processes, each of which could materially and adversely affect its business, financial condition and results of operations. | |

| ● | Stryve may not be able to compete successfully in the highly competitive snacking and nutritional snacking industry. | |

| ● | Stryve may face direct competition in the future from well-capitalized competitors. | |

| ● | Stryve’s brand and reputation may be diminished due to real or perceived quality or health issues with its products, including meat, which could materially and adversely affect its business, financial condition and results of operations. | |

| ● | If Stryve fails to implement its growth strategies successfully, timely, or at all, its ability to increase revenue and achieve profitability could be materially and adversely affected. | |

| ● | If Stryve fails to effectively manage its manufacturing and production capacity, its business and operating results and brand reputation could be harmed. | |

| ● | Most of Stryve’s products are manufactured in its single facility in Oklahoma and any damage to or disruption at this facility would materially and adversely affect its business, financial condition and results of operations. | |

| ● | Beef, raw material and packaging costs can be volatile and may rise significantly, which may negatively impact the ability of Stryve to achieve profitability. | |

| ● | Stryve relies on a limited number of third-party suppliers, and may not be able to obtain beef and other raw materials on a timely basis or in sufficient quantities to produce its products or meet the demand for its products. | |

| ● | Stryve relies on sales to a limited number of retailers and losing one or more such retailers could materially and adversely affect its business, financial condition and results of operations. | |

| ● | Consolidation of customers or the loss of a significant customer could negatively impact Stryve’s sales and ability to achieve profitability. | |

| ● | Stryve’s growth may be limited if it is unable to add additional shelf or retail space for its products. | |

| ● | Changes in retail distribution arrangements may result in the temporary loss of retail shelf space and disrupt sales of food products which could materially and adversely affect Stryve’s business, financial condition and results of operations. | |

| ● | Slotting fees and customer charges or charge-backs for promotion allowances, cooperative advertising, and product or packaging damages, as well as undelivered or unsold food products may disrupt Stryve’s customer relationships and could materially and adversely affect its business, financial condition and results of operations. |

| 9 |